Rabobank's new World Vegetable Map illustrates global vegetable trade flows and highlights recent trends from a turbulent sector – from increasing global trade to volatile consumer prices, decreasing EU production, and rising US imports.

Click here to download the World Vegetable Map 2024.

Click here to download the World Vegetable Map 2024.

The past five years have been anything but boring for the vegetable sector. The Covid-19 pandemic, extreme weather events, skyrocketing costs for growers, and challenging logistics are just some factors that have impacted the sector. Our recently published World Vegetable Map reflects some of these disruptions, for example, in the remarkably high global trade in 2021 and the roller-coaster ride of consumer vegetable prices. Most of the pictured trends, however, are rather long-term developments. Mexico, Spain, and the Netherlands have remained relevant exporters in the world of fresh vegetables, and countries such as Turkey and Poland are becoming bigger producers and exporters of both fresh and processed vegetables.

EU and US vegetable production decreasing

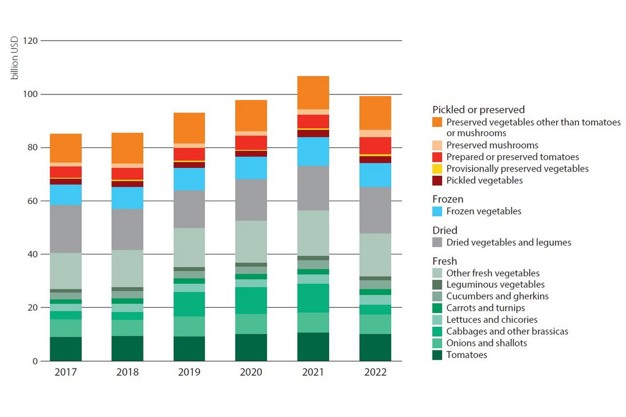

An estimated 7% of vegetables produced globally are traded, either fresh or processed, mainly within continents and often between neighboring countries. From 2017 to 2022, global trade in both processed and fresh vegetables increased by an average of 3% per year, though not in a linear pattern due to the Covid pandemic and the subsequent global wave of inflation (see figure 1). Global vegetable production grew at a slower pace of 1.2% per year. Notably, the EU and the US both experienced declines in production by 3.6% and 3.3% a year, respectively, in the period from 2017 to 2022.

Figure 1: Global vegetable trade, 2017-2022  US increasingly dependent on imported vegetables

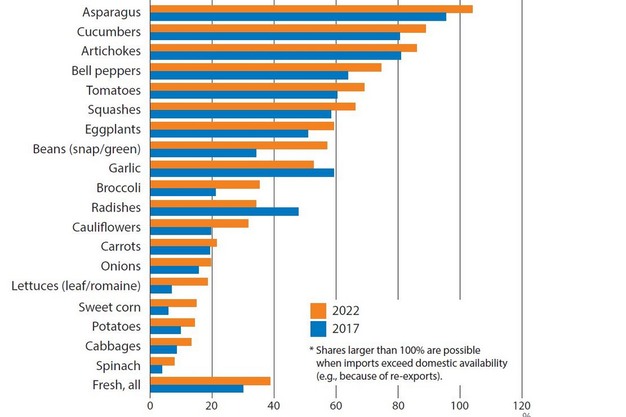

US increasingly dependent on imported vegetables

During the last five years, the US reinforced its position as the world's largest import market for fresh vegetables. The country's share of imports for greenhouse vegetables such as cucumbers, tomatoes, and bell peppers is particularly high (see figure 2). Due to ongoing strong demand from the US, Mexico's total fresh vegetable exports increased by almost 40% between 2017 and 2022.

Figure 2: Share of imported vegetables in total fresh vegetables available in the US, 2017 vs. 2022

A mixed bag of European vegetable imports

Spain, the Netherlands, and Italy have remained important exporters to other EU countries and the UK for fresh and processed vegetables. However, Morocco, Poland, and Turkey have increased their presence in the European fresh vegetable market. Poland increased its exports and imports.

Seeds: A small input of high importance

Starting with high-quality materials is key for producers of quality vegetables. The Netherlands has strengthened its position in the breeding and trading of high-value vegetable seeds. Chile also holds a unique position in seed production and exports due to its natural conditions and Southern Hemisphere location. The US is both a large exporter and importer of vegetable seeds.

Click here to download the full Rabobank PDF article.

For more information:

Cindy van Rijswick

Rabobank

Email: [email protected]