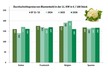

The commercial greenhouse market is expanding rapidly, driven by increased demand for ornamentals, year-round produce, and locally grown plants. In fact, the North America commercial greenhouse market size was valued at $5.9 billion in 2024, and is projected to reach $11.4 billion by 2031.

As the number of greenhouse growing operations rises throughout the country, finding an insurance provider who knows the horticultural industry and its unique risks—no matter where you set up shop—can help ensure your coverages make sense for your business.

Whether you're growing plants, flowers, fruits, or vegetables within a traditional greenhouse or a renovated warehouse, insurance for greenhouse growers plays a major role in helping support the financial well-being of your business.

What unique risks do greenhouses face?

You provide a variety of plants and services that your customers count on. Don't let an unforeseen hazard ruin that relationship. Every greenhouse operation faces risk exposures that businesses in other industries often don't—and which may not be covered under a standard business insurance policy. The characteristics of your operation alone can influence your exposures, such as using glass, polycarbonate, plastic, or fiberglass cladding, selling plugs or finished products and producing potted plants, vegetables, fruits, or specialty cuts.

Help protect your passion and your business by staying vigilant and proactively managing your risks.

Crop losses

Whether it's flowers or other plants, your crop could be put in jeopardy if a climate control system fails. Commercial property insurance helps cover crop losses for plants grown in climate-controlled structures. It can even help cover your future crop income if you can't plant due to damage.

Storm damage

Every greenhouse faces the threat of hail, lightning, high winds, and tornadoes. Depending on where your business is located, there's also the danger of hurricanes and heavy snow. Significant storm damage repairs can be expensive and delay how quickly you can get your business up and running again. Property insurance can help protect you when storm damage affects your operations and can help you minimize losses.

Electrical fires

Devastating fires to greenhouse property are sometimes caused by poor or deteriorating electrical connections and wiring. A fire within your greenhouse could disrupt operations and result in prolonged downtime. Some insurance providers can use thermal imaging to help identify possible electrical problems. Business interruption insurance can help cover additional expenses to keep your operations running and help supplement lost income if your business is disrupted.

Equipment breakdowns

When your equipment breaks down, it can mean weeks of lost productivity and lost revenue. Equipment breakdown coverage can help reduce your costs and get your operations back on track.

Slips, trips, and falls

Hoses, wet floors, and ladders are commonly found around greenhouse walkways and can lead to costly injuries and workers' compensation claims. Your insurance provider can work with you to minimize the risks around your workplace to help keep employees and customers safe.

What are the benefits of greenhouse insurance?

As covered above, your greenhouse faces unique risks every day. When losses do occur, greenhouse insurance can provide your business financial protection so the financial burden of paying for damages doesn't fall entirely on you, helping you keep your business running.

In addition, your business insurance provider can help with risk mitigation strategies and help ensure you comply with state insurance regulations.

© Hortica

© Hortica

Essential insurance coverages for greenhouse businesses

When insuring your greenhouses, you want your coverage tailored to their size, scope, and region. Larger operations often select higher deductibles and higher umbrella limits to reflect their increased exposure.

Weather is also a determining factor: growers in cold and snowy climates have different considerations than growers in warm climates. If a boiler breaks at a greenhouse in Minnesota, it's usually a more immediate concern than if a boiler breaks at a greenhouse in Florida.

As a business owner, you don't want to risk being underinsured if you face a claim. Keep in mind, not all states require the same insurance coverages, but consider the following coverages and discuss these with your provider:

Tips for selecting a greenhouse insurance provider

With new and alternative commercial growing operations on the rise, it's important to choose an insurer that understands the nuances and unique challenges of the horticultural industry.

Hortica®, a brand of the Sentry Insurance Group, has been serving the horticultural industry for more than 135 years. We have a deep understanding of the horticultural environment, its risks, and how to help protect your business.

For more information: Hortica

Hortica

www.hortica.com