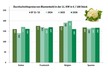

French tomato production for the fresh market is estimated (according to forecasts drawn up on September 1st, 2025) at 504,300 tons for the 2025 season, which is slightly higher than in 2024 (+1%). In August 2025, against a backdrop of a temporary drop in volumes in the southern basins and weather that favored consumption, prices were 10% higher than in 2024 and 29% higher than the 2020-2024 average for the same month.

Production up in southern basins throughout the season

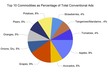

The national area sown to tomatoes for the fresh market in the 2025 marketing year is slightly lower than last year (-1%), at 2,767 hectares. However, it will still be 2% higher than the 2020-2024 average. French tomato production for the fresh market is estimated at 504,300 tons in 2025, 1% higher than last year, with some contrasts depending on the basin. Production dropped in the west of the country (-6%) and in the Centre-West and West basins (-3%). On the other hand, production increased in the south (+6%) and in the South-West and South-East basins (+5%). Production in 2025 is also 1% higher than the average for 2020-2024, due to production in the South-West basin being well above the five-year average (+18%).

French supply was high in June and July. In August, the very hot weather caused a dip in production in the south of the country. Weather conditions were milder in the Centre-West region, but the drop in acreage weighed on production levels.

Marketing: good value since June

In May, the market was fairly buoyant at the start of the month, but it was affected at the end of the month by a lack of outlets, with reduced consumption due to bad weather and a large number of berry imports. In June, supply was good, and the more favorable weather boosted demand, enabling the product to be sold at a good price (+31% from last year and +13% compared to the 2020-2024 average for the same month). In July, the market remained buoyant with sustained demand. In August, trade intensified, boosting the value of production, facilitated by a temporarily reduced supply in the southern basins. Prices picked up sharply and then dropped at the end of August, with a resumption of supply in the southern basins.

Between January and July 2025 and compared with the same period last year, tomato exports (171,100 tons), including significant volumes of re-exports, dropped by 15% and imports (335,500 tons) by 9%. The foreign trade deficit in volume terms (164,400 tons) dropped by 2% from last year during the period under review.

Source: Agreste