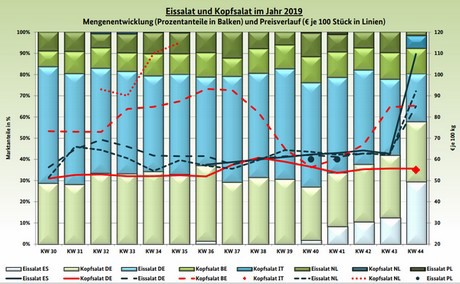

In the case of iceberg lettuce, Spanish shipments were predominant. The Dutch and local season turned into the home straight: The quality of the goods weakened and the inflow was limited. Price quotes for rare and popular consumer items rose. Despite the high prices, they were simply scooped up. In Frankfurt, even the Spanish products were in short supply, as the supply was restricted by effects like rain in the growing regions as well as fixed quantities within the retail trade. At times, €17 per 10-piece box had to be paid there.

In the case of lettuce, the overall condition of domestic offers was increasingly getting less good. This was the reason why Belgian greenhouse goods then came into focus. The sizes of these were quite mixed in Munich, resulting in a wide range of prices.

It was here that the first Italian lots arrived, in wooden boxes of twelve, which cost about as much as the German batches. For colorful salads, local shipments could easily cover the demand. Italian suppliers tried to gain market share. Traders saw little reason to change their prices, because of continuous business.

Domestic endives became a lot cheaper in Munich, which accelerated their sales. In Frankfurt, meanwhile, Italian goods supplemented the product range, that was dominated by Germany. The availability of Belgian and local lamb's lettuce was in line with demand, so that prices generally remained at their current level.

Apples

Almost all places reported lower prices, especially with regard to local fruits. This was done for different reasons; the autumn holidays played a role, as well as the rainy weather and the associated drop in demand.

Pears

The pear trade was calm and without highlights. Supply and demand were often in balance. Changes in prices were very rare.

Table grapes

Although Italian supplies became narrower, they still shaped the market. First and foremost were the Thompson Seedless, Italia and Crimson Seedless. Greece participated with Thompson Seedless and Crimson Seedless, Turkey primarily with Sultana.

Small citrus fruits

Clementines were sold predominantly. These came from Spain and Italy. With Clemenules, Marisol, Clemenrubi and Oronules some varieties were ready. The organoleptic properties were good overall.

Lemons

Spanish Primofiori prevailed. The demand was satisfied without difficulty. The prices remained stable. Here and there they dropped, resulting in brisker sales.

Bananas

In general, although calm sales were reported, they were relatively continuous. The autumn holiday period often reduced sales opportunities.

Cauliflower

Germany evidently shaped the scene. Demand grew locally, but this was not a problem since availability was sufficient to meet it.

Cucumbers

The demand could be satisfied without difficulty. However, sales were not always smooth, as popularity had slowed as a result of the autumn holidays.

Tomatoes

In general, demand was disappointing at several places; it could be satisfied quite easily. The prices developed unevenly.

Sweet peppers

Spain prevailed here. The Netherlands and Turkey came next. The supply was mostly harmonized with the demand.